Spyder_ Final

- 1. Cisco Martinez September, 27 2011 Spyder Active Sports, Inc.

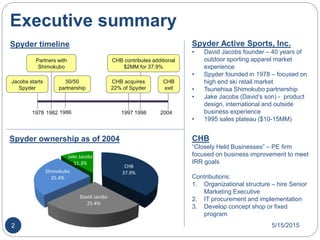

- 2. Executive summary 1978 19861982 1997 1998 2004 Jacobs starts Spyder Partners with Shimokubo 50/50 partnership CHB acquires 22% of Spyder CHB contributes additional $2MM for 37.9% CHB exit CHB 37.9% David Jacobs 25.4% Shimokubo 25.4% Jake Jacobs 11.3% Spyder timeline Spyder ownership as of 2004 Spyder Active Sports, Inc. ŌĆó David Jacobs founder ŌĆō 40 years of outdoor sporting apparel market experience ŌĆó Spyder founded in 1978 ŌĆō focused on high end ski retail market ŌĆó Tsunehisa Shimokubo partnership ŌĆó Jake Jacobs (DavidŌĆÖs son) - product design, international and outside business experience ŌĆó 1995 sales plateau ($10-15MM) CHB ŌĆ£Closely Held BusinessesŌĆØ ŌĆō PE firm focused on business improvement to meet IRR goals Contributions: 1. Organizational structure ŌĆō hire Senior Marketing Executive 2. IT procurement and implementation 3. Develop concept shop or fixed program 5/15/20152

- 3. Decisions for Spyder ŌĆó What is the FirmŌĆÖs Value? ŌĆó Strategic Acquirer or Financial Acquirer? ŌĆó Total Company or Minority Stake? 5/15/20153

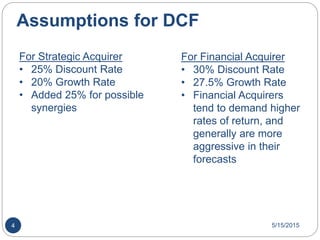

- 4. Assumptions for DCF For Financial Acquirer ŌĆó 30% Discount Rate ŌĆó 27.5% Growth Rate ŌĆó Financial Acquirers tend to demand higher rates of return, and generally are more aggressive in their forecasts For Strategic Acquirer ŌĆó 25% Discount Rate ŌĆó 20% Growth Rate ŌĆó Added 25% for possible synergies 5/15/20154

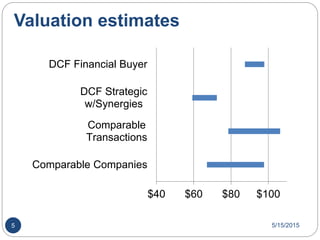

- 5. Valuation estimates $40 $60 $80 $100 Comparable Companies Comparable Transactions DCF Strategic w/Synergies DCF Financial Buyer 5/15/20155

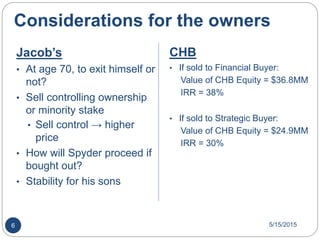

- 6. Considerations for the owners CHB ŌĆó If sold to Financial Buyer: Value of CHB Equity = $36.8MM IRR = 38% ŌĆó If sold to Strategic Buyer: Value of CHB Equity = $24.9MM IRR = 30% JacobŌĆÖs ŌĆó At age 70, to exit himself or not? ŌĆó Sell controlling ownership or minority stake ŌĆó Sell control ŌåÆ higher price ŌĆó How will Spyder proceed if bought out? ŌĆó Stability for his sons 5/15/20156

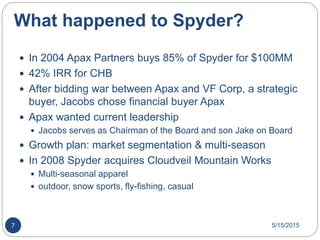

- 7. What happened to Spyder? ’éŚ In 2004 Apax Partners buys 85% of Spyder for $100MM ’éŚ 42% IRR for CHB ’éŚ After bidding war between Apax and VF Corp, a strategic buyer, Jacobs chose financial buyer Apax ’éŚ Apax wanted current leadership ’éŚ Jacobs serves as Chairman of the Board and son Jake on Board ’éŚ Growth plan: market segmentation & multi-season ’éŚ In 2008 Spyder acquires Cloudveil Mountain Works ’éŚ Multi-seasonal apparel ’éŚ outdoor, snow sports, fly-fishing, casual 5/15/20157

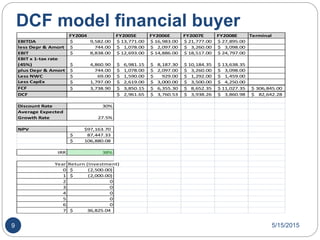

- 9. DCF model financial buyer FY2004 FY2005E FY2006E FY2007E FY2008E Terminal EBITDA 9,582.00$ 13,771.00$ 16,983.00$ 21,777.00$ 27,895.00$ less Depr & Amort 744.00$ 1,078.00$ 2,097.00$ 3,260.00$ 3,098.00$ EBIT 8,838.00$ 12,693.00$ 14,886.00$ 18,517.00$ 24,797.00$ EBIT x 1-tax rate (45%) 4,860.90$ 6,981.15$ 8,187.30$ 10,184.35$ 13,638.35$ plus Depr & Amort 744.00$ 1,078.00$ 2,097.00$ 3,260.00$ 3,098.00$ Less NWC 69.00$ 1,590.00$ 929.00$ 1,292.00$ 1,459.00$ Less CapEx 1,797.00$ 2,619.00$ 3,000.00$ 3,500.00$ 4,250.00$ FCF 3,738.90$ 3,850.15$ 6,355.30$ 8,652.35$ 11,027.35$ 306,845.00$ DCF 2,961.65$ 3,760.53$ 3,938.26$ 3,860.98$ 82,642.28$ Discount Rate 30% Average Expected Growth Rate 27.5% NPV $97,163.70 87,447.33$ 106,880.08$ IRR 38% Year Return (Investment) 0 (2,500.00)$ 1 (2,000.00)$ 2 0 3 0 4 0 5 0 6 0 7 36,825.04$ 5/15/20159

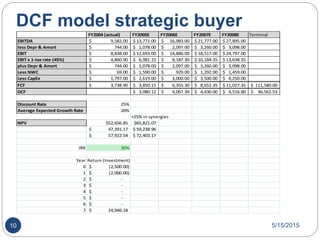

- 10. DCF model strategic buyer FY2004 (actual) FY2005E FY2006E FY2007E FY2008E Terminal EBITDA 9,582.00$ 13,771.00$ 16,983.00$ 21,777.00$ 27,895.00$ less Depr & Amort 744.00$ 1,078.00$ 2,097.00$ 3,260.00$ 3,098.00$ EBIT 8,838.00$ 12,693.00$ 14,886.00$ 18,517.00$ 24,797.00$ EBIT x 1-tax rate (45%) 4,860.90$ 6,981.15$ 8,187.30$ 10,184.35$ 13,638.35$ plus Depr & Amort 744.00$ 1,078.00$ 2,097.00$ 3,260.00$ 3,098.00$ Less NWC 69.00$ 1,590.00$ 929.00$ 1,292.00$ 1,459.00$ Less CapEx 1,797.00$ 2,619.00$ 3,000.00$ 3,500.00$ 4,250.00$ FCF 3,738.90$ 3,850.15$ 6,355.30$ 8,652.35$ 11,027.35$ 111,580.00$ DCF 3,080.12$ 4,067.39$ 4,430.00$ 4,516.80$ 36,562.53$ Discount Rate 25% Average Expected Growth Rate 20% +25% in synergies NPV $52,656.85 $65,821.07 47,391.17$ 59,238.96$ 57,922.54$ 72,403.17$ IRR 30% Year Return (Investment) 0 (2,500.00)$ 1 (2,000.00)$ 2 -$ 3 -$ 4 -$ 5 -$ 6 -$ 7 24,946.18$ 5/15/201510

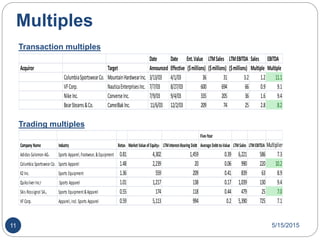

- 11. Multiples Date Date Ent.Value LTMSales LTMEBITDA Sales EBITDA Acquiror Target Announced Effective ($millions) ($millions) ($millions) Multiple Multiple ColumbiaSportswearCo. MountainHardwearInc. 3/13/03 4/1/03 36 31 3.2 1.2 11.1 VFCorp. NauticaEnterprisesInc. 7/7/03 8/27/03 600 694 66 0.9 9.1 NikeInc. ConverseInc. 7/9/03 9/4/03 335 205 36 1.6 9.4 BearStearns&Co. CameIBakInc. 11/6/03 12/2/03 209 74 25 2.8 8.2 Transaction multiples Trading multiples Five-Year Company Name Industry Betab MarketValueofEquityc LTMInterest-Bearing Debt AverageDebt-to-Value LTMSales LTMEBITDA Multiplier Adidas-Salomon AGd Sports Apparel,Footwear,&Equipment 0.81 4,302 1,459 0.39 6,221 586 7.3 Columbia SportswearCo. Sports Apparel 1.48 2,239 20 0.06 990 220 10.2 K2Inc. Sports Equipment 1.36 559 209 0.41 839 63 8.9 QuiksilverInc.f Sports Apparel 1.01 1,217 138 0.17 1,039 130 9.4 Skis Rossignol SA.g Sports Equipment&Apparel 0.55 174 118 0.44 479 25 7.0 VF Corp. Apparel,incl.Sports Apparel 0.59 5,113 994 0.2 5,390 725 7.1 5/15/201511