Accounting in action (Chapter-1) in Accounting ppt

Download as PPTX, PDF4 likes2,647 views

Accounting in action for slideshare Accounting in action(Chapter-1) in Accounting Accounting in action (Chapter-1) in Accounting ppt By Sadia akter

1 of 30

Downloaded 83 times

Recommended

Chapter 1: Accounting in Action

Chapter 1: Accounting in Actiontepsokha

╠²

1) The document discusses accounting principles and provides examples of accounting transactions for a computer programming business called Softbyte.

2) Softbyte's owner, Marc Doucet, invests $15,000 to start the business and purchases $7,000 of computer equipment. Softbyte also buys supplies on account.

3) The accounting equation and building blocks are explained. Revenues, expenses, assets, liabilities and owner's equity are defined and various transactions are analyzed to demonstrate how they affect the accounting equation.Introduction to Financial statements - Accounting

Introduction to Financial statements - AccountingFaHaD .H. NooR

╠²

Financial statement introduction and its elements.

There are three fundamental financial statements used in accounting.

The income statement shows revenues and expenses.

The balance sheet is a listing of all asset, liability, and equity account balances that do not appear on the income statement.

The statement of cash flows shows how the company receives and spends its cash. Cash Flow Statement

Cash Flow StatementRajaKrishnan M

╠²

This document provides information on management accounting and cash flow statements. It defines management accounting as the presentation and analysis of business information for internal management decision making. It then defines a cash flow statement as a financial statement showing the changes in cash and cash equivalents resulting from operating, investing, and financing activities. The objectives of the cash flow statement are to present the inflows and outflows of cash over a period and to help evaluate a company's liquidity, dividend-paying capacity, and reasons for changes in cash balances. Advantages include assessing liquidity and profitability, determining optimal cash balances, and aiding capital budgeting decisions.Financial statement of non - profit organisation

Financial statement of non - profit organisationGHSS Chavakkad

╠²

Non-profit organizations are established to provide services rather than earn profits. They are organized for social, educational, religious, or charitable purposes. Their main objectives are to serve members and society without trading or earning profits. Financial statements for non-profits include a receipts and payments account, income and expenditure account, and balance sheet. The receipts and payments account summarizes all cash receipts and payments, while the income and expenditure account records revenue and expenses to determine any surplus or deficit. The balance sheet presents assets, capital or fund balances, and liabilities at a point in time.| Accounting Cycle | Double Entry Accounting | Basic Accounting Equation | 8 ...

| Accounting Cycle | Double Entry Accounting | Basic Accounting Equation | 8 ...Ahmad Hassan

╠²

Principles of accounting, the accounting cycle, double entry accounting, debits and credits, basic accounting equation, ownership structure, steps in accounting cycle, transactions and events, journalizing, techniques of journalizing, posting, trial balance, adjusting entries, classes of adjusting entries, adjusted trial balance, preparing financial statements, closing entries, post-closing trial balance financial accounting

financial accounting pooja Devi(Guru Nanak dev University)

╠²

Accounting is the process of identifying, measuring, recording, classifying, summarizing, analyzing, interpreting and communicating financial information about an entity. It involves recording economic events which affect the financial position and performance of a business. The key functions of accounting include identifying transactions, measuring transactions in monetary terms, recording transactions methodically in books of accounts, classifying transactions into appropriate accounts, summarizing transactions periodically into financial statements, analyzing trends and relationships, interpreting financial statements for decision making and communicating essential information to users.Journal,Ledger and Trial Balance

Journal,Ledger and Trial Balancezahid6

╠²

The document describes journal entries, ledger accounts, and a trial balance for a business called Campus Laundromat. It provides details of transactions during the first month of operations in September 2017, including an owner investment of $20,000 cash, $1,000 paid for rent, $1,200 paid for insurance, and $700 withdrawn for personal use. Journal entries are made for each transaction and ledger accounts are opened and balanced. A trial balance at September 30, 2017 lists the balances of each account.Journal ledger and trial balance

Journal ledger and trial balanceFahim Muntaha

╠²

The document summarizes journal and ledger posting concepts and procedures. It provides examples of journal entries for capital contributions by partners and transactions involving cash, purchases, sales, and other accounts. It then explains the key aspects of ledger accounts including their format and the posting process to transfer journal entries to respective accounts in the ledger. Procedures for compound journal entries and advantages of the ledger are also outlined.1.14 Assets

1.14 AssetsVCE Accounting - Michael Allison

╠²

VCE Accounting Unit 3. Video of this presentation can be found on my YouTube channel here https://www.youtube.com/channel/UCf5jyuJoYwie8tWfvjEc0zg. Correction of accounting errors

Correction of accounting errorsSanjaya Jayasundara

╠²

Correction of Accounting Errors chapter can be easily understand by using this presentation. Sanjaya Jayasundara08

08Khalid Aziz

╠²

(1) The Allowance for Doubtful Accounts is a contra-asset account subtracted from accounts receivable on the balance sheet.

(2) The actual write-off entry does not reduce net receivables.

(3) The estimation error inherent in the allowance method is more acceptable than violating the matching principle with the direct write-off method.Treasury organization & structure

Treasury organization & structureKrishal Gwachha

╠²

- Treasury departments are structured differently depending on a company's size and complexity, ranging from one person to multiple divisions.

- They typically have three main divisions: front office for daily transactions/risk management, middle office for independent risk monitoring and reporting, and back office for validation, settlement, accounting.

- The front office includes dealers and traders who take positions and manage market risks. The middle office monitors exposures and reports to management. The back office confirms deals and handles bookkeeping. An audit team also inspects daily operations.Introduction to accounting

Introduction to accountingVishal Kukreja

╠²

This document provides an introduction to the concepts of accounting. It defines accounting as a system that collects and processes financial information to allow informed decisions by users. It discusses the need for accounting to determine results of business transactions and the financial position. It outlines the key functions of accounting like identifying, recording, classifying, summarizing, analyzing, interpreting and communicating financial information. It also discusses the accounting cycle and different branches and users of accounting information. Finally, it provides definitions of some basic accounting terms.Basic accounting principles

Basic accounting principlesUmar Gul

╠²

The document discusses key accounting principles including the four main financial statements, the basic accounting equation, and different types of accounts. It also covers topics like accrual versus cash accounting, depreciation, financial analysis methods, and financial ratios used to evaluate business performance and health. The document is intended to provide an overview of basic accounting concepts.As 17 presentation 1

As 17 presentation 1nitingoyal_143

╠²

This document outlines Accounting Standard 17 on segment reporting in India. It defines key terms like business segment, geographical segment, segment revenue, expenses, assets and liabilities. It provides guidelines on identifying reportable segments based on a 10% threshold of revenue, profits, assets or liabilities. Enterprises must disclose segment revenues, results, assets, liabilities and other details for all reportable segments.19.1 - Cash vs accrual accounting

19.1 - Cash vs accrual accountingVCE Accounting - Michael Allison

╠²

- There are two main methods for determining profit - cash accounting and accrual accounting. Cash accounting only recognizes revenue and expenses when cash is received or paid, while accrual accounting recognizes revenue when earned and expenses when incurred regardless of cash flow.

- Accrual accounting provides a more accurate measure of net profit as it aligns revenues with related expenses over the appropriate reporting periods based on the principles of going concern, reporting period, and relevance. This allows expenses like depreciation and prepaid expenses to be allocated to the correct periods.Ch06 accounting for merchandising business, intro accounting, 21st edition ...

Ch06 accounting for merchandising business, intro accounting, 21st edition ...Trisdarisa Soedarto, MPM, MQM

╠²

This document discusses accounting for merchandising businesses. It begins by distinguishing the activities and financial statements of service businesses from merchandising businesses. It then describes the accounting treatment for various merchandising transactions including sales, purchases, transportation costs, and discounts. Specific topics covered include the perpetual and periodic inventory methods, income statements, statements of owner's equity, balance sheets, journal entries for cash, credit and discount sales, and accounting for the costs of goods sold. The objectives are to understand how to account for the key activities of a merchandising business.Control accounts

Control accountsSanjaya Jayasundara

╠²

Control accounts the account which represents a particular sub ledger, sales ledger and purchases ledger control accounts.

At the end of an accounting period the accounts are balanced off and a trial balance prepared to check the accuracy of the book keeping entries. If a trial balance fails to balance this usually indicates that an error or errors may have been made and needs to be identified. As the business expands the accounting requirements increase which may lead to more errors occurring which are very difficult to find.

Types of accounts

Types of accountsDr Khyati Boriya -BDS (MHA)

╠²

The document discusses accounting concepts and the accounting cycle. It defines accounting as a tool for decision making. It distinguishes between financial and management accounting based on their users. It also describes the key components of the accounting cycle including journalizing transactions, the general journal, debit and credit rules, and how the double-entry system ensures equal debits and credits.Topic 5 ledger

Topic 5 ledgerSrinivas Methuku

╠²

The document discusses the meaning, contents, and purpose of ledgers in accounting. It explains that a ledger is the principal book of accounts that contains all personal, real, and nominal accounts from the journal. Transactions are posted from the journal to the relevant accounts in the ledger. Accounts are balanced by determining the difference between total debits and credits, and the ledger provides a complete record of business transactions and accounting information. Examples are given of ledger layout, posting entries, and balancing accounts.Final accounts

Final accounts Ankit Sand

╠²

- The document discusses key steps in the accounting process including preparing trial balance, final accounts (trading account, profit & loss account, balance sheet), and various adjustments needed for the financial statements.

- It provides examples and explanations of key final account components like trading account, profit & loss account, balance sheet, and adjustments for closing stock, outstanding expenses, prepaid expenses, accrued income, and more.

- The purpose is to explain how to close accounts and prepare final financial statements that show the profit/loss for the period and current financial position.The accounting equation

The accounting equationMickyM05

╠²

The accounting equation shows that assets and liabilities of a company are equal. It is based on the dual concept that every transaction has two effects - a debit and a credit. Assets are possessions that result in economic resources flowing into the business, while liabilities are debts that result in outflows. Owners' equity represents the owners' claim on assets. To prepare an accounting equation, transactions are analyzed in terms of their impact on assets, liabilities, expenses and owners' equity, and the relevant accounts are adjusted. An example shows a business owner investing cash, increasing both the asset and owners' equity accounts by the same amount.Trend analysis

Trend analysisAnagha Gokhale

╠²

This document discusses various types of financial statement analysis including trend analysis, comparative statements, common size statements, and ratio analysis. It provides templates for comparative balance sheets and income statements showing calculations of amount and percentage changes between periods. It also includes templates for common size statements showing items as a percentage of total capital employed or net sales. Financial statement analysis is used to measure profitability, growth, financial strength, and solvency by analyzing relationships and trends over time from financial statements.Accrual Accounting and Balance Day Adjustments

Accrual Accounting and Balance Day AdjustmentsCollege

╠²

The document discusses different accounting methods and balance day adjustments. It describes cash accounting and accrual accounting. It then explains four common balance day adjustments - prepaid expenses, accrued expenses, unearned revenues, and accrued revenues - through examples and journal entries. These adjustments ensure revenues and expenses are accurately matched between accounting periods.Fixed Assets Accounting

Fixed Assets AccountingWe Learn - A Continuous Learning Forum from Welingkar's Distance Learning Program.

╠²

Fixed Assets Accounting is very essential for matching costs with revenues. A fixed asset is an asset held with the intention of being used for producing goods. Check the above presentation for in-depth details.

For more such innovative content on management studies, join WeSchool PGDM-DLP Program: http://bit.ly/║▌║▌▀ŻshareFaccounting

Join us on Facebook: http://www.facebook.com/welearnindia

Follow us on Twitter: https://twitter.com/WeLearnIndia

Read our latest blog at: http://welearnindia.wordpress.com

Subscribe to our ║▌║▌▀Żshare Channel: http://www.slideshare.net/welingkarDLPCh 8 - Accounting for Receivables.ppt

Ch 8 - Accounting for Receivables.pptTutorialOnline2

╠²

This document provides an overview of accounting for receivables. It defines different types of receivables like accounts receivable and notes receivable. It explains how companies recognize, value, and dispose of both accounts receivable and notes receivable. Specific topics covered include recognizing revenue on credit sales, estimating and recording allowance for doubtful accounts, accounting for uncollectible accounts, determining maturity dates and interest on notes, and presenting receivables on financial statements. The document aims to help students understand the key accounting concepts and entries related to receivables.Financial statements.

Financial statements.Sushil kasar

╠²

The document discusses financial accounting concepts like trading accounts, profit and loss accounts, and using accounting information systems. It defines trading accounts and explains their purpose is to calculate gross profit or loss. It also defines profit and loss accounts and how they are used to determine net profit. The document recommends using accounting information systems to automate financial statements for increased accuracy and efficiency over manual methods. It describes the components, benefits, and common types of accounting information systems.Cambridge o level introduction to accounting

Cambridge o level introduction to accountingSanjaya Jayasundara

╠²

Cambridge O level

Accounting

7707

Introduction to Accounting

Business Entity Concept

Business point of view

Accounting Equation

Assets

Capital/ Equity

Liabilities

Double Entry System

Dual Effect Conceptch01-Session 1 2.ppt

ch01-Session 1 2.pptMadeinBangladesh1

╠²

1. The document discusses the basic concepts and principles of accounting, including what accounting is, the accounting process, and the key parties interested in accounting information.

2. It explains the basic building blocks of accounting - assets, liabilities, owner's equity, revenues and expenses. Assets are resources owned, liabilities are debts owed, and owner's equity is the claim on assets by the owner.

3. The basic accounting equation is introduced as Assets = Liabilities + Owner's Equity, and the key types of business organizations - proprietorship, partnership, and corporation - are defined.Financial Accounting .pptx

Financial Accounting .pptxRobbia Rana

╠²

This document defines accounting and outlines its primary functions and users. It discusses how accounting involves recording business transactions, summarizing results into reports, and providing assurance. Accounting aids decision making by showing how money is spent and the implications of different plans. Financial statements like the income statement and balance sheet are key outputs. The accounting cycle and double-entry bookkeeping are also summarized.More Related Content

What's hot (20)

1.14 Assets

1.14 AssetsVCE Accounting - Michael Allison

╠²

VCE Accounting Unit 3. Video of this presentation can be found on my YouTube channel here https://www.youtube.com/channel/UCf5jyuJoYwie8tWfvjEc0zg. Correction of accounting errors

Correction of accounting errorsSanjaya Jayasundara

╠²

Correction of Accounting Errors chapter can be easily understand by using this presentation. Sanjaya Jayasundara08

08Khalid Aziz

╠²

(1) The Allowance for Doubtful Accounts is a contra-asset account subtracted from accounts receivable on the balance sheet.

(2) The actual write-off entry does not reduce net receivables.

(3) The estimation error inherent in the allowance method is more acceptable than violating the matching principle with the direct write-off method.Treasury organization & structure

Treasury organization & structureKrishal Gwachha

╠²

- Treasury departments are structured differently depending on a company's size and complexity, ranging from one person to multiple divisions.

- They typically have three main divisions: front office for daily transactions/risk management, middle office for independent risk monitoring and reporting, and back office for validation, settlement, accounting.

- The front office includes dealers and traders who take positions and manage market risks. The middle office monitors exposures and reports to management. The back office confirms deals and handles bookkeeping. An audit team also inspects daily operations.Introduction to accounting

Introduction to accountingVishal Kukreja

╠²

This document provides an introduction to the concepts of accounting. It defines accounting as a system that collects and processes financial information to allow informed decisions by users. It discusses the need for accounting to determine results of business transactions and the financial position. It outlines the key functions of accounting like identifying, recording, classifying, summarizing, analyzing, interpreting and communicating financial information. It also discusses the accounting cycle and different branches and users of accounting information. Finally, it provides definitions of some basic accounting terms.Basic accounting principles

Basic accounting principlesUmar Gul

╠²

The document discusses key accounting principles including the four main financial statements, the basic accounting equation, and different types of accounts. It also covers topics like accrual versus cash accounting, depreciation, financial analysis methods, and financial ratios used to evaluate business performance and health. The document is intended to provide an overview of basic accounting concepts.As 17 presentation 1

As 17 presentation 1nitingoyal_143

╠²

This document outlines Accounting Standard 17 on segment reporting in India. It defines key terms like business segment, geographical segment, segment revenue, expenses, assets and liabilities. It provides guidelines on identifying reportable segments based on a 10% threshold of revenue, profits, assets or liabilities. Enterprises must disclose segment revenues, results, assets, liabilities and other details for all reportable segments.19.1 - Cash vs accrual accounting

19.1 - Cash vs accrual accountingVCE Accounting - Michael Allison

╠²

- There are two main methods for determining profit - cash accounting and accrual accounting. Cash accounting only recognizes revenue and expenses when cash is received or paid, while accrual accounting recognizes revenue when earned and expenses when incurred regardless of cash flow.

- Accrual accounting provides a more accurate measure of net profit as it aligns revenues with related expenses over the appropriate reporting periods based on the principles of going concern, reporting period, and relevance. This allows expenses like depreciation and prepaid expenses to be allocated to the correct periods.Ch06 accounting for merchandising business, intro accounting, 21st edition ...

Ch06 accounting for merchandising business, intro accounting, 21st edition ...Trisdarisa Soedarto, MPM, MQM

╠²

This document discusses accounting for merchandising businesses. It begins by distinguishing the activities and financial statements of service businesses from merchandising businesses. It then describes the accounting treatment for various merchandising transactions including sales, purchases, transportation costs, and discounts. Specific topics covered include the perpetual and periodic inventory methods, income statements, statements of owner's equity, balance sheets, journal entries for cash, credit and discount sales, and accounting for the costs of goods sold. The objectives are to understand how to account for the key activities of a merchandising business.Control accounts

Control accountsSanjaya Jayasundara

╠²

Control accounts the account which represents a particular sub ledger, sales ledger and purchases ledger control accounts.

At the end of an accounting period the accounts are balanced off and a trial balance prepared to check the accuracy of the book keeping entries. If a trial balance fails to balance this usually indicates that an error or errors may have been made and needs to be identified. As the business expands the accounting requirements increase which may lead to more errors occurring which are very difficult to find.

Types of accounts

Types of accountsDr Khyati Boriya -BDS (MHA)

╠²

The document discusses accounting concepts and the accounting cycle. It defines accounting as a tool for decision making. It distinguishes between financial and management accounting based on their users. It also describes the key components of the accounting cycle including journalizing transactions, the general journal, debit and credit rules, and how the double-entry system ensures equal debits and credits.Topic 5 ledger

Topic 5 ledgerSrinivas Methuku

╠²

The document discusses the meaning, contents, and purpose of ledgers in accounting. It explains that a ledger is the principal book of accounts that contains all personal, real, and nominal accounts from the journal. Transactions are posted from the journal to the relevant accounts in the ledger. Accounts are balanced by determining the difference between total debits and credits, and the ledger provides a complete record of business transactions and accounting information. Examples are given of ledger layout, posting entries, and balancing accounts.Final accounts

Final accounts Ankit Sand

╠²

- The document discusses key steps in the accounting process including preparing trial balance, final accounts (trading account, profit & loss account, balance sheet), and various adjustments needed for the financial statements.

- It provides examples and explanations of key final account components like trading account, profit & loss account, balance sheet, and adjustments for closing stock, outstanding expenses, prepaid expenses, accrued income, and more.

- The purpose is to explain how to close accounts and prepare final financial statements that show the profit/loss for the period and current financial position.The accounting equation

The accounting equationMickyM05

╠²

The accounting equation shows that assets and liabilities of a company are equal. It is based on the dual concept that every transaction has two effects - a debit and a credit. Assets are possessions that result in economic resources flowing into the business, while liabilities are debts that result in outflows. Owners' equity represents the owners' claim on assets. To prepare an accounting equation, transactions are analyzed in terms of their impact on assets, liabilities, expenses and owners' equity, and the relevant accounts are adjusted. An example shows a business owner investing cash, increasing both the asset and owners' equity accounts by the same amount.Trend analysis

Trend analysisAnagha Gokhale

╠²

This document discusses various types of financial statement analysis including trend analysis, comparative statements, common size statements, and ratio analysis. It provides templates for comparative balance sheets and income statements showing calculations of amount and percentage changes between periods. It also includes templates for common size statements showing items as a percentage of total capital employed or net sales. Financial statement analysis is used to measure profitability, growth, financial strength, and solvency by analyzing relationships and trends over time from financial statements.Accrual Accounting and Balance Day Adjustments

Accrual Accounting and Balance Day AdjustmentsCollege

╠²

The document discusses different accounting methods and balance day adjustments. It describes cash accounting and accrual accounting. It then explains four common balance day adjustments - prepaid expenses, accrued expenses, unearned revenues, and accrued revenues - through examples and journal entries. These adjustments ensure revenues and expenses are accurately matched between accounting periods.Fixed Assets Accounting

Fixed Assets AccountingWe Learn - A Continuous Learning Forum from Welingkar's Distance Learning Program.

╠²

Fixed Assets Accounting is very essential for matching costs with revenues. A fixed asset is an asset held with the intention of being used for producing goods. Check the above presentation for in-depth details.

For more such innovative content on management studies, join WeSchool PGDM-DLP Program: http://bit.ly/║▌║▌▀ŻshareFaccounting

Join us on Facebook: http://www.facebook.com/welearnindia

Follow us on Twitter: https://twitter.com/WeLearnIndia

Read our latest blog at: http://welearnindia.wordpress.com

Subscribe to our ║▌║▌▀Żshare Channel: http://www.slideshare.net/welingkarDLPCh 8 - Accounting for Receivables.ppt

Ch 8 - Accounting for Receivables.pptTutorialOnline2

╠²

This document provides an overview of accounting for receivables. It defines different types of receivables like accounts receivable and notes receivable. It explains how companies recognize, value, and dispose of both accounts receivable and notes receivable. Specific topics covered include recognizing revenue on credit sales, estimating and recording allowance for doubtful accounts, accounting for uncollectible accounts, determining maturity dates and interest on notes, and presenting receivables on financial statements. The document aims to help students understand the key accounting concepts and entries related to receivables.Financial statements.

Financial statements.Sushil kasar

╠²

The document discusses financial accounting concepts like trading accounts, profit and loss accounts, and using accounting information systems. It defines trading accounts and explains their purpose is to calculate gross profit or loss. It also defines profit and loss accounts and how they are used to determine net profit. The document recommends using accounting information systems to automate financial statements for increased accuracy and efficiency over manual methods. It describes the components, benefits, and common types of accounting information systems.Cambridge o level introduction to accounting

Cambridge o level introduction to accountingSanjaya Jayasundara

╠²

Cambridge O level

Accounting

7707

Introduction to Accounting

Business Entity Concept

Business point of view

Accounting Equation

Assets

Capital/ Equity

Liabilities

Double Entry System

Dual Effect ConceptCh06 accounting for merchandising business, intro accounting, 21st edition ...

Ch06 accounting for merchandising business, intro accounting, 21st edition ...Trisdarisa Soedarto, MPM, MQM

╠²

Fixed Assets Accounting

Fixed Assets AccountingWe Learn - A Continuous Learning Forum from Welingkar's Distance Learning Program.

╠²

Similar to Accounting in action (Chapter-1) in Accounting ppt (20)

ch01-Session 1 2.ppt

ch01-Session 1 2.pptMadeinBangladesh1

╠²

1. The document discusses the basic concepts and principles of accounting, including what accounting is, the accounting process, and the key parties interested in accounting information.

2. It explains the basic building blocks of accounting - assets, liabilities, owner's equity, revenues and expenses. Assets are resources owned, liabilities are debts owed, and owner's equity is the claim on assets by the owner.

3. The basic accounting equation is introduced as Assets = Liabilities + Owner's Equity, and the key types of business organizations - proprietorship, partnership, and corporation - are defined.Financial Accounting .pptx

Financial Accounting .pptxRobbia Rana

╠²

This document defines accounting and outlines its primary functions and users. It discusses how accounting involves recording business transactions, summarizing results into reports, and providing assurance. Accounting aids decision making by showing how money is spent and the implications of different plans. Financial statements like the income statement and balance sheet are key outputs. The accounting cycle and double-entry bookkeeping are also summarized.

01_TheRoleofAccounting_FinancialAccounting.pptx

01_TheRoleofAccounting_FinancialAccounting.pptxwanasyiqin1

╠²

Accounting is the process of identifying, measuring, recording, and communicating financial information about an entity. It allows businesses to answer key questions like how they are performing financially and making decisions. The basic accounting equation is Assets = Liabilities + Owner's Equity, which must always balance. Transactions affect accounts and this equation. There are challenges like ethics and standards that governing bodies address.Financial analysis.docx

Financial analysis.docxZeyad43

╠²

Finance for Managers

(Managerial Accounting)

Role of Financial Information

ŌĆó Financial information pervades our economy

ŌĆō It is the primary means of communication between profit seeking

organizations and their stakeholders

ŌĆō For this reason organizations use financial measures internally as a broad indicator of performance

ŌĆó This financial information provides a signal that something is wrong, but not what is wrong

ŌĆó Financial information summarizes underlying activities

ŌĆō But to explain financial results, managers need to dig deeper

ŌĆō Detailed information provides additional insight into what is happening to

profits

AccountingforNon-AccountantsPresentation.pptx

AccountingforNon-AccountantsPresentation.pptxIrishBogacia2

╠²

This document outlines an accounting course covering fundamental accounting concepts and financial statements. The course objectives are to understand accounting information sources and concepts, how financial data is used for decision making, and controlling operations. Topics include the balance sheet, income statement, cash flows, accounting principles, corporations, and ratio analysis. The course utilizes lectures, assignments, cases, and exams. Managerial accounting is also covered, focusing on cost analysis, budgeting, and decision making.FA.pptx

FA.pptxuday231983

╠²

The document provides an overview of basic financial accounting concepts including the definition of accounts, accounting principles and processes, types of accounts and ledgers, the accounting cycle, and key accounting terminology. It also discusses the different bases, systems, and branches of accounting as well as the advantages, limitations, and users of accounting information.Types of accounts basic accounting -concepts prepared by Prof.Satish R.Tajane

Types of accounts basic accounting -concepts prepared by Prof.Satish R.TajaneDr. Satish Tajane

╠²

This document provides an overview of accounting concepts and principles including:

- The major distinction between financial and management accounting and their users.

- The basic relationships in the decision making process that accountants analyze and record transactions.

- The key components of the balance sheet including assets, liabilities, and owner's equity.

- The double entry accounting system and how transactions are analyzed and recorded in journals using debit and credit rules for different types of accounts.Basics of Accounting

Basics of AccountingDevashish Pandey

╠²

Accounting is a system for measuring and recording business transactions and reporting financial information. It involves processing transactions, preparing financial statements, and providing information to decision-makers. The key points are:

- Accounting records business transactions, prepares financial reports like the income statement and balance sheet, and provides information to managers, investors, and others.

- Accounting principles and conventions provide guidelines for financial reporting and include concepts like business entity, cost, matching, and consistency to ensure uniformity and comparability.

- Management accounting provides internal reports for decision-making while financial accounting prepares external financial statements for stakeholders.Cb12e basic ppt ch16

Cb12e basic ppt ch16Eric

╠²

Accounting involves measuring, interpreting, and communicating financial information to support business decision making. It plays a key role in financing, investing, and operating activities of businesses. There are various types of accountants including public, management, government, and not-for-profit accountants. The accounting process converts transaction information into financial statements using principles like GAAP. Financial statements including the balance sheet, income statement, and statement of cash flows provide information on a business's financial position and performance.Accounting basics .pptx

Accounting basics .pptxMostafaGamal216952

╠²

This chapter discusses the fundamentals of accounting including its nature, functions, users, principles, and key concepts. Accounting identifies, records, and communicates the financial events of a business. It provides information to internal users like managers and external users like investors and creditors. Companies follow generally accepted accounting principles to prepare four main financial statements - the income statement, balance sheet, statement of owner's equity, and statement of cash flows. The accounting equation forms the basis of recording transactions and showing a company's assets, liabilities, and owner's equity.Basics of financial accounting

Basics of financial accountingVisakhapatnam

╠²

This document provides an overview of basic financial accounting concepts. It defines key accounting terms like accounts, accounting, the accounting cycle and basis. It describes the different types of accounts, rules of double entry system and branches of accounting. It also explains the accounting process including journal, ledger, trial balance and errors. The accounting concepts, conventions and terminology are introduced along with the different books of accounts used.

Finacial accounting

Finacial accountingGjergjmihilli

╠²

Real estate is something that you can physically touch and feel ŌĆō it's a real good and, therefore, for many financiar ,feels more real. Maybe this partially accounts for the high return on the venture, as from 1978-2004, real estate has had an average return of 8.6%. For many time this investment has generated consistent wealth and long term respect for millions of people.

FINANCIAL ACCOUNTING

FINANCIAL ACCOUNTINGTrinity Dwarka

╠²

Every decision that a business makes has financial implications and any decision that affects the finances of a business is a significant decision.lec 1 Introduction of Financial Accounting.pptx

lec 1 Introduction of Financial Accounting.pptxssuseraf82a0

╠²

Accounting is the process of recording financial transactions pertaining to a business in terms of money. There are two main types of accounting: management accounting, which analyzes costs and operations to aid decision making, and financial accounting, which prepares financial statements to show a company's financial performance and position to external users. Financial accounting practice follows generally accepted accounting principles (GAAP) to provide information that is relevant, reliable, and comparable.Language of business

Language of businessAziz Fataliyev, Internal Audit Practitioner

╠²

Basics of Accounting. Terminology, definition of Statements and examples of double entry in terms of commercial Bank.Chapter 13 accounting concepts, professional judgments,aand ethical conduct

Chapter 13 accounting concepts, professional judgments,aand ethical conductNoman Khilji

╠²

This document discusses accounting concepts, professional judgments, and ethical conduct in accounting. It covers the need for recognized accounting standards and generally accepted accounting principles (GAAP). GAAP provide ground rules for financial reporting and include concepts like the accounting entity, going concern assumption, time period principle, and stable dollar assumption. It also discusses asset valuation, revenue recognition, matching principle, consistency principle, disclosure principle, materiality, conservatism, audited financial statements, setting new accounting standards, and professional codes of ethics. Accountants have unique ethical responsibilities to serve the public interest.chapter on principle.ppt

chapter on principle.pptGirmaNegash1

╠²

This chapter introduces accounting concepts and principles. It describes the nature of business and accounting's role in providing financial information. Accounting involves identifying, measuring, recording, and communicating financial transactions and is the language of business. The accounting equation, assets = liabilities + equity, expresses the relationship between what a business owns, owes, and is worth. The chapter also discusses the accounting cycle, from recording transactions to producing financial statements, and the accounts used to track changes in a business's financial position and performance.Recently uploaded (20)

US Patented ReGenX Generator, ReGen-X Quatum Motor EV Regenerative Accelerati...

US Patented ReGenX Generator, ReGen-X Quatum Motor EV Regenerative Accelerati...Thane Heins NOBEL PRIZE WINNING ENERGY RESEARCHER

╠²

Preface: The ReGenX Generator innovation operates with a US Patented Frequency Dependent Load Current Delay which delays the creation and storage of created Electromagnetic Field Energy around the exterior of the generator coil. The result is the created and Time Delayed Electromagnetic Field Energy performs any magnitude of Positive Electro-Mechanical Work at infinite efficiency on the generator's Rotating Magnetic Field, increasing its Kinetic Energy and increasing the Kinetic Energy of an EV or ICE Vehicle to any magnitude without requiring any Externally Supplied Input Energy. In Electricity Generation applications the ReGenX Generator innovation now allows all electricity to be generated at infinite efficiency requiring zero Input Energy, zero Input Energy Cost, while producing zero Greenhouse Gas Emissions, zero Air Pollution and zero Nuclear Waste during the Electricity Generation Phase. In Electric Motor operation the ReGen-X Quantum Motor now allows any magnitude of Work to be performed with zero Electric Input Energy.

Demonstration Protocol: The demonstration protocol involves three prototypes;

1. Protytpe #1, demonstrates the ReGenX Generator's Load Current Time Delay when compared to the instantaneous Load Current Sine Wave for a Conventional Generator Coil.

2. In the Conventional Faraday Generator operation the created Electromagnetic Field Energy performs Negative Work at infinite efficiency and it reduces the Kinetic Energy of the system.

3. The Magnitude of the Negative Work / System Kinetic Energy Reduction (in Joules) is equal to the Magnitude of the created Electromagnetic Field Energy (also in Joules).

4. When the Conventional Faraday Generator is placed On-Load, Negative Work is performed and the speed of the system decreases according to Lenz's Law of Induction.

5. In order to maintain the System Speed and the Electric Power magnitude to the Loads, additional Input Power must be supplied to the Prime Mover and additional Mechanical Input Power must be supplied to the Generator's Drive Shaft.

6. For example, if 100 Watts of Electric Power is delivered to the Load by the Faraday Generator, an additional >100 Watts of Mechanical Input Power must be supplied to the Generator's Drive Shaft by the Prime Mover.

7. If 1 MW of Electric Power is delivered to the Load by the Faraday Generator, an additional >1 MW Watts of Mechanical Input Power must be supplied to the Generator's Drive Shaft by the Prime Mover.

8. Generally speaking the ratio is 2 Watts of Mechanical Input Power to every 1 Watt of Electric Output Power generated.

9. The increase in Drive Shaft Mechanical Input Power is provided by the Prime Mover and the Input Energy Source which powers the Prime Mover.

10. In the Heins ReGenX Generator operation the created and Time Delayed Electromagnetic Field Energy performs Positive Work at infinite efficiency and it increases the Kinetic Energy of the system.Frankfurt University of Applied Science urkunde

Frankfurt University of Applied Science urkundeLisa Emerson

╠²

Duplicate Frankfurt University of Applied Science urkunde, make a Frankfurt UAS degree.Taykon-Kalite belgeleri

Taykon-Kalite belgeleriTAYKON

╠²

Kalite Politikam─▒z

Taykon ├ćelik i├¦in kalite, hayallerinizi bizlerle payla┼¤t─▒─¤─▒n─▒z an ba┼¤lar. Proje ├¦iziminden detaylar─▒n ├¦├Čz├╝m├╝ne, detaylar─▒n ├¦├Čz├╝m├╝nden ├╝retime, ├╝retimden montaja, montajdan teslime hayallerinizin ger├¦ekle┼¤ti─¤ini g├Črd├╝─¤├╝n├╝z ana kadar ge├¦en t├╝m a┼¤amalar─▒, ├¦al─▒┼¤anlar─▒, t├╝m teknik donan─▒m ve ├¦evreyi i├¦ine al─▒r KAL─░TE.Integration of Additive Manufacturing (AM) with IoT : A Smart Manufacturing A...

Integration of Additive Manufacturing (AM) with IoT : A Smart Manufacturing A...ASHISHDESAI85

╠²

Combining 3D printing with Internet of Things (IoT) enables the creation of smart, connected, and customizable objects that can monitor, control, and optimize their performance, potentially revolutionizing various industries. oT-enabled 3D printers can use sensors to monitor the quality of prints during the printing process. If any defects or deviations from the desired specifications are detected, the printer can adjust its parameters in real time to ensure that the final product meets the required standards.

Sachpazis: Foundation Analysis and Design: Single Piles

Sachpazis: Foundation Analysis and Design: Single PilesDr.Costas Sachpazis

╠²

Žü. ╬ÜŽÄŽāŽä╬▒Žé ╬Ż╬▒ŽćŽĆ╬¼╬Č╬ĘŽé: Foundation Analysis and Design: Single Piles

Welcome to this comprehensive presentation on "Foundation Analysis and Design," focusing on Single PilesŌĆöStatic Capacity, Lateral Loads, and Pile/Pole Buckling. This presentation will explore the fundamental concepts, equations, and practical considerations for designing and analyzing pile foundations.

We'll examine different pile types, their characteristics, load transfer mechanisms, and the complex interactions between piles and surrounding soil. Throughout this presentation, we'll highlight key equations and methodologies for calculating pile capacities under various conditions.15. Smart Cities Big Data, Civic Hackers, and the Quest for a New Utopia.pdf

15. Smart Cities Big Data, Civic Hackers, and the Quest for a New Utopia.pdfNgocThang9

╠²

Smart Cities Big Data, Civic Hackers, and the Quest for a New UtopiaEnv and Water Supply Engg._Dr. Hasan.pdf

Env and Water Supply Engg._Dr. Hasan.pdfMahmudHasan747870

╠²

Core course, namely Environment and Water Supply Engineering. Full lecture notes are in book format for the BSc in Civil Engineering program. Optimization of Cumulative Energy, Exergy Consumption and Environmental Life ...

Optimization of Cumulative Energy, Exergy Consumption and Environmental Life ...J. Agricultural Machinery

╠²

Optimal use of resources, including energy, is one of the most important principles in modern and sustainable agricultural systems. Exergy analysis and life cycle assessment were used to study the efficient use of inputs, energy consumption reduction, and various environmental effects in the corn production system in Lorestan province, Iran. The required data were collected from farmers in Lorestan province using random sampling. The Cobb-Douglas equation and data envelopment analysis were utilized for modeling and optimizing cumulative energy and exergy consumption (CEnC and CExC) and devising strategies to mitigate the environmental impacts of corn production. The Cobb-Douglas equation results revealed that electricity, diesel fuel, and N-fertilizer were the major contributors to CExC in the corn production system. According to the Data Envelopment Analysis (DEA) results, the average efficiency of all farms in terms of CExC was 94.7% in the CCR model and 97.8% in the BCC model. Furthermore, the results indicated that there was excessive consumption of inputs, particularly potassium and phosphate fertilizers. By adopting more suitable methods based on DEA of efficient farmers, it was possible to save 6.47, 10.42, 7.40, 13.32, 31.29, 3.25, and 6.78% in the exergy consumption of diesel fuel, electricity, machinery, chemical fertilizers, biocides, seeds, and irrigation, respectively. UNIT 1FUNDAMENTALS OF OPERATING SYSTEMS.pptx

UNIT 1FUNDAMENTALS OF OPERATING SYSTEMS.pptxKesavanT10

╠²

UNIT 1FUNDAMENTALS OF OPERATING SYSTEMS.pptxAI, Tariffs and Supply Chains in Knowledge Graphs

AI, Tariffs and Supply Chains in Knowledge GraphsMax De Marzi

╠²

How tarrifs, supply chains and knowledge graphs combine.

How Engineering Model Making Brings Designs to Life.pdf

How Engineering Model Making Brings Designs to Life.pdfMaadhu Creatives-Model Making Company

╠²

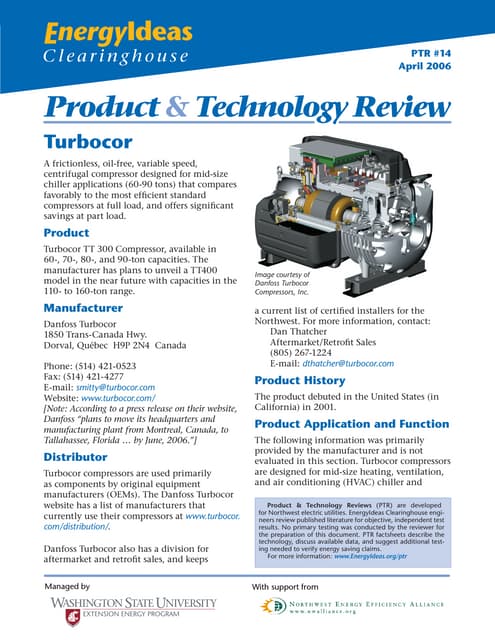

This PDF highlights how engineering model making helps turn designs into functional prototypes, aiding in visualization, testing, and refinement. It covers different types of models used in industries like architecture, automotive, and aerospace, emphasizing cost and time efficiency.Turbocor Product and Technology Review.pdf

Turbocor Product and Technology Review.pdfTotok Sulistiyanto

╠²

High Efficiency Chiller System in HVACUnit II: Design of Static Equipment Foundations

Unit II: Design of Static Equipment FoundationsSanjivani College of Engineering, Kopargaon

╠²

Design of Static Equipment, that is vertical vessels foundation.US Patented ReGenX Generator, ReGen-X Quatum Motor EV Regenerative Accelerati...

US Patented ReGenX Generator, ReGen-X Quatum Motor EV Regenerative Accelerati...Thane Heins NOBEL PRIZE WINNING ENERGY RESEARCHER

╠²

Optimization of Cumulative Energy, Exergy Consumption and Environmental Life ...

Optimization of Cumulative Energy, Exergy Consumption and Environmental Life ...J. Agricultural Machinery

╠²

Accounting in action (Chapter-1) in Accounting ppt

- 2. Accounting in Action Sadia Akter

- 4. ŌĆó Accounting is an information system that ŌĆó Identifies ŌĆó Records ŌĆó Communicates the economic events of an organization to interested users WHAT IS ACCOUNTING? Sadia Akter

- 6. QUESTIONS ASKED BY INTERNAL USERS

- 7. QUESTIONS ASKED BY EXTERNAL USERS

- 8. BOOKKEEPING DISTINGUISHED FROM ACCOUNTING ŌĆó Accounting Includes bookkeeping Also includes much more ŌĆó Bookkeeping The recording of economic events One part of accounting

- 9. THE ACCOUNTING PROFESSION ŌĆó Public Accountants Service to the general public through the services they perform. ŌĆó Private Accountants Individuals in companies involved in activities including cost and tax accounting, systems, and internal auditing. ŌĆó Not For Profit Accountants Reporting and control for government units, foundations, hospitals, labor unions, colleges/universities, and charities.

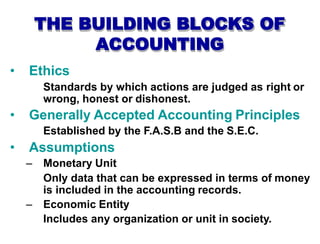

- 10. THE BUILDING BLOCKS OF ACCOUNTING ŌĆó Ethics Standards by which actions are judged as right or wrong, honest or dishonest. ŌĆó Generally Accepted Accounting Principles Established by the F.A.S.B and the S.E.C. ŌĆó Assumptions ŌĆō Monetary Unit Only data that can be expressed in terms of money is included in the accounting records. ŌĆō Economic Entity Includes any organization or unit in society.

- 11. BASIC ACCOUNTING EQUATION Assets Liabilities OwnerŌĆÖs Equity= +

- 12. ASSETS AS A BUILDING BLOCK ŌĆó Assets are resources owned by a business. ŌĆó They are used in carrying out such activities as production, consumption and exchange.

- 13. LIABILITIES AS A BUILDING BLOCK ŌĆó Liabilities ŌĆó are creditor claims against assets ŌĆó are existing debts and obligations

- 14. ŌĆó OwnerŌĆÖs Equity = total assets minus total liabilities. (A - L = O.E.) ŌĆó OwnerŌĆÖs Equity represents the ownership claim to total assets. ŌĆó Subdivisions of OwnerŌĆÖs Equity: 1 Capital or Investments by Owner (+) 2 Drawing (-) 3 Revenues (+) 4 Expenses (-) OWNERŌĆÖS EQUITY AS A BUILDING BLOCK

- 15. INCREASES AND DECREASES IN OWNERŌĆÖS EQUITY ŌĆóINCREASES DECREASES Investments by Owner Revenues OwnerŌĆÖs Equity Withdrawals by Owner Expenses

- 25. FINANCIAL STATEMENTS ŌĆóFour financial statements are prepared from the summarized accounting data: ŌĆó Income Statement revenues and expenses and resulting net income or net loss for a specific period of time ŌĆó OwnerŌĆÖs Equity Statement changes in ownerŌĆÖs equity for a specific period of time ŌĆó Balance Sheet assets, liabilities, and ownerŌĆÖs equity at a specific date

- 26. FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS

- 27. FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS

- 28. FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS

- 29. Any Question?

- 30. Thanks